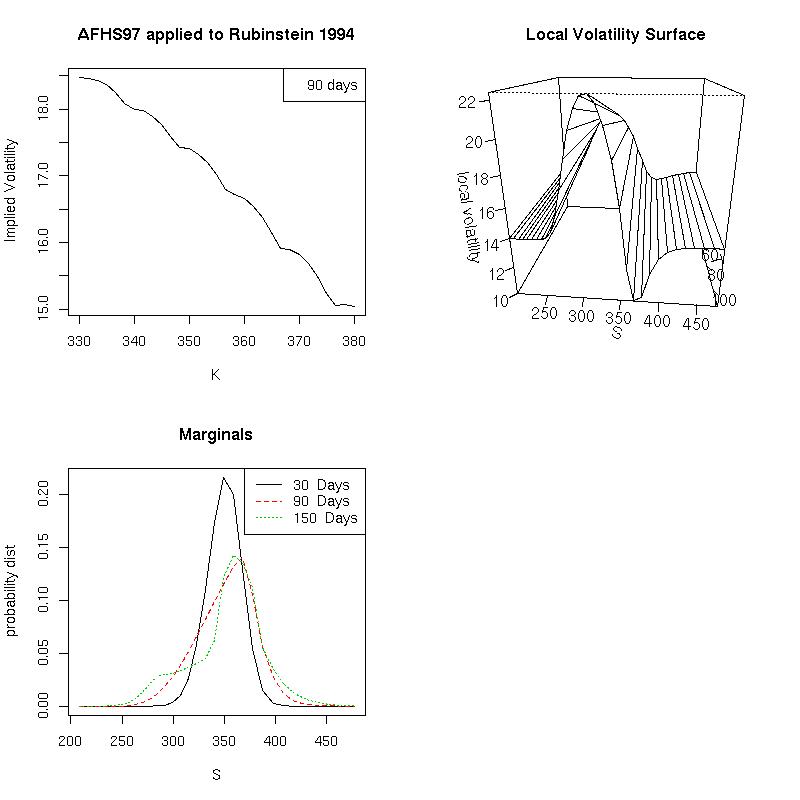

Calibrates a diffusion pricing model using the methodology AFHS97,

where the prices are taken from Rubinstein 1994 (option prices for

a single maturity). The 90-day implied volatility curve is shown, along

with the implied local volatility surface and the marginals. The

150-day marginal suggests "crash-o-phobia".