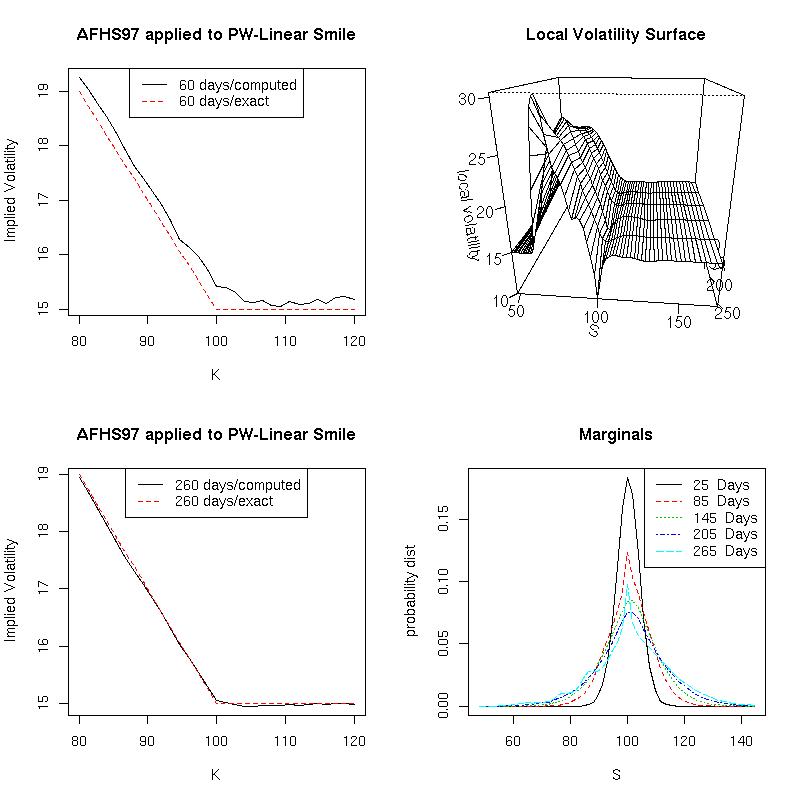

Calibrates a diffusion pricing model using the methodology AFHS97,

where the prices are sampled from an (almost) piecewise-linear

implied volatility surface. 60-day and 260-day implied volatilities are compared

with the input (exact) curves, and the local volatility

surface and marginals are also shown.